Chaikin Money Flow + MACD + ATRHere I present you on of Trade Pro's Trading Idea: Chaikin Money Flow + MACD + ATR.

This strategy is not as profitable as it can be seen in one of his videos. In the forex market, the strategy could reach a maximum of 35% profitability.

I have, as some of my followers have requested, created an overview of the current position, risk and leverage settings in the form of a table.

Furthermore, one can again swap between short and long positions.

It is now possible to select or deselect individual indicators.

I have chosen the ATR alone as a take profit stop loss, as in his strategy.

A position is only triggered as soon as all prerequisites have been fulfilled and a command is executed. This prevents false triggering by bots and repainting.

-----------------------------------------------------------------------------------

How does the strategy work?

ENTRY

Long

The MACD indicator must be above the zero line.

Then the K line must cross the D line.

Finally, when this happens, the Money Flow Index must be above the zero line.

Short

Contrary to the premise of long positions.

EXIT

ATR Exit

The value of ATR at the time of buying is multiplied by the value entered in "Profit factor ATR" and "Stop factor ATR". As soon as the price reaches this value, it is closed.

Important

The script must be optimized for each coin or currency pair.

I will publish a guide to the strategy shortly. There I will explain how the table works and how to set the strategy correctly.

The results of the strategy are without commissions and leverage.

If you have any questions or feedback, please let me know in the comments.

ابحث في النصوص البرمجية عن "profit factor"

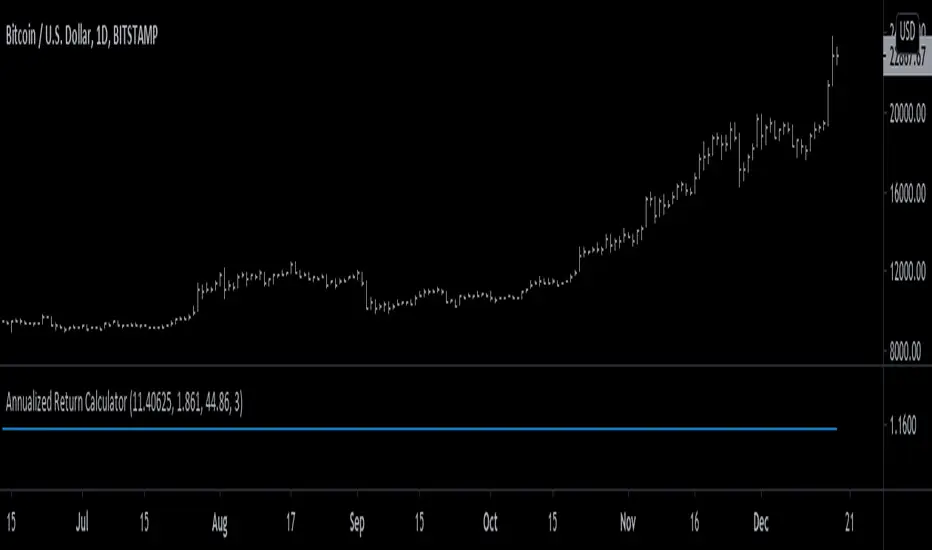

Strategy's Annual Return [racer8]I was trying to find the annual return for a particular strategy script based on profit factor, annual trade frequency, and win rate.

So on paper, I created some equations to help me solve this...and eventually, I created this indicator!

This indicator will help you find the annual return for any strategy. All you need to input is profit factor, number of trades per year, and win rate...oh and percentage of equity to risk in the trades.

By the way, if the output is 1.15, that means 15% annual return.

Keep in mind that this is a mere approximation...and the actual return is likely lower than this value.

Also if your margin trading, set order size to 100% of equity in the strategy's parameters.

Hopes this helps. Good luck and enjoy ;)

Bitcoin - MA Crossover StrategyBefore You Begin:

Please read these warnings carefully before using this script, you will bear all fiscal responsibility for your own trades.

Trading Strategy Warning - Past performance of this strategy may not equal future performance, due to macro-environment changes, etc.

Account Size Warning - Performance based upon default 10% risk per trade, of account size $100,000. Adjust BEFORE you trade to see your own drawdown.

Time Frame - D1 and H4. H4 has a lower profit factor (more fake-outs, and account drawdown), D1 recommended.

Trend Following System - Profitability of this system is dependent on STRONG future trends in Bitcoin (BTCUSD).

Default Settings:

This script was tested on Daily and 4 Hourly charts using the following default settings. Note that 4 Hourly exhibits higher drawdowns and lower profit factor, whilst Daily appears more stable.

Account Size ($): 100,000 (please adjust to simulate your own risk)

Equity Risk (%): 10 (please adjust to simulate your own risk)

Fast Moving Average (Period): 20

Slow Moving Average (Period): 40

Relative Strength Index (Period): 14

Trading Mechanism:

Trend following strategies work well for assets that display the tendency of long-trends. Please do not use this script on financial assets that have a historical tendency for mean reversion. Bitcoin has historically exhibited strong trends, and thus this script is designed to capitalise on that behaviour. It is hoped (but we cannot predict), that Bitcoin will strongly trend in the coming days.

LONG:

Enter Long - When fast moving average (20) crosses ABOVE slow moving average (40)

Exit Long - When fast moving average (20) crosses BELOW slow moving average (40)

SHORT:

Enter Short - When fast moving average (20) crosses BELOW slow moving average (40)

Exit Short - When fast moving average (20) crosses ABOVE slow moving average (40)

Risk Warnings:

Do note that "moving averages" are a lagging indicator, and as such heavy drawdowns could occur when a trade is open. If you are trading this system manually, it is best to avoid emotions and let the system tell you when to enter and exit. Do not panic and exit manually when under heavy drawdown, always follow the system. Do not be emotional. If possible, connect this to your broker for auto-trading. Ensure that your risk per trade (Equity Risk) is SMALL enough that it does not result in a margin-call on your trading account. Equity risk must always be considered relative to your total account size.

Remember: You bear all financial responsibility for your trades, best of luck.

Volume Weighted Bollinger Bands Strategy

Simple strategy,

Using Volume weighted Bollinger Bands

> Directions for Usage:

1. Use only in scripts where volume is specified by tradingview

2. Check on which timeframe the script has a profit factor greater than 1.4

3. Use that timeframe for profitability

4. In some high liquid securities there is a decent profit factor even at 5 min scale (optimise at your end!! all i want to say)

Enjoy!

Hope this helps!!

[XC] Adaptive strategy with volume bandsFirst much thanks to alexgrover for his rich source of unbelievable indicators

The list below shows as an example some might profitable strategy settings.

But like every new strategy only a long term test can tell you if it works.

//Curency - - src Time stategy Length C. Factor Smoothed SL TP Profit Factor (with no Commission)

//---------------------------------------------------------------------------------------------------------------------------------

//BTCUSD NOHA close 15min 1 240 10 yes 3000 25000 4.2 (June 2019)

//XBTUSD NOHA close 15min 1 310 0.00006 no 1000 11000 2.3 (June 2019)

//IOTABTC NOHA close 15min 1 380 0.0004 no 2000 11000 10.6 (June 2019)

ISM Indicator As a Strategy Here's a very easy code, plotting the ISM against the SPX. In this exercise, i wanted to see if one could use the ISM indicator only to generate buy/sell signal, and what would be the performance.

What is the ISM

The ISM Manufacturing Index monitors employment, production inventories, new orders and supplier deliveries.By monitoring the ISM Manufacturing Index, investors are able to better understand national economic conditions. When this index is increasing, investors can assume that the stock markets should increase because of higher corporate profits. The opposite can be thought of the bond markets, which may decrease as the ISM Manufacturing Index increases because of sensitivity to potential inflation.

Buy/Sell Signal

ISM above 50 usually good economic condition and vice versa when below 50 . For this code I used 48.50 as my buy/sell signal line.

Results

To test this on a longer time period, I use the SPX index instead of SPY. The results are surprisingly good. 76.92% profitability with 3.03 profit factor.

Conclusion

Investors could use the ISM with other indicators to determine better entry and exit point. I will see if combining the ISM with other custom indicators , could generate better result. Feel free to share your results here.

Cheers

Algo.

Hilly's Advanced Crypto Scalping Strategy - 5 Min ChartTo determine the "best" input parameters for the Advanced Crypto Scalping Strategy on a 5-minute chart, we need to consider the goals of optimizing for profitability, minimizing false signals, and adapting to the volatile nature of cryptocurrencies. The default parameters in the script are a starting point, but the optimal values depend on the specific cryptocurrency pair, market conditions, and your risk tolerance. Below, I'll provide recommended input values based on common practices in crypto scalping, along with reasoning for each parameter. I’ll also suggest how to fine-tune them using TradingView’s backtesting and optimization tools.

Recommended Input Parameters

These values are tailored for a 5-minute chart for liquid cryptocurrencies like BTC/USD or ETH/USD on exchanges like Binance or Coinbase. They aim to balance signal frequency and accuracy for day trading.

Fast EMA Length (emaFastLen): 9

Reasoning: A 9-period EMA is commonly used in scalping to capture short-term price movements while remaining sensitive to recent price action. It reacts faster than the default 10, aligning with the 5-minute timeframe.

Slow EMA Length (emaSlowLen): 21

Reasoning: A 21-period EMA provides a good balance for identifying the broader trend on a 5-minute chart. It’s slightly longer than the default 20 to reduce noise while confirming the trend direction.

RSI Length (rsiLen): 14

Reasoning: The default 14-period RSI is a standard choice for momentum analysis. It works well for detecting overbought/oversold conditions without being too sensitive on short timeframes.

RSI Overbought (rsiOverbought): 75

Reasoning: Raising the overbought threshold to 75 (from 70) reduces false sell signals in strong bullish trends, which are common in crypto markets.

RSI Oversold (rsiOversold): 25

Reasoning: Lowering the oversold threshold to 25 (from 30) filters out weaker buy signals, ensuring entries occur during stronger reversals.

MACD Fast Length (macdFast): 12

Reasoning: The default 12-period fast EMA for MACD is effective for capturing short-term momentum shifts in crypto, aligning with scalping goals.

MACD Slow Length (macdSlow): 26

Reasoning: The default 26-period slow EMA is a standard setting that works well for confirming momentum trends without lagging too much.

MACD Signal Smoothing (macdSignal): 9

Reasoning: The default 9-period signal line is widely used and provides a good balance for smoothing MACD crossovers on a 5-minute chart.

Bollinger Bands Length (bbLen): 20

Reasoning: The default 20-period Bollinger Bands are effective for identifying volatility breakouts, which are key for scalping in crypto markets.

Bollinger Bands Multiplier (bbMult): 2.0

Reasoning: A 2.0 multiplier is standard and captures most price action within the bands. Increasing it to 2.5 could reduce signals but improve accuracy in highly volatile markets.

Stop Loss % (slPerc): 0.8%

Reasoning: A tighter stop loss of 0.8% (from 1.0%) suits the high volatility of crypto, helping to limit losses on false breakouts while keeping risk manageable.

Take Profit % (tpPerc): 1.5%

Reasoning: A 1.5% take-profit target (from 2.0%) aligns with scalping’s goal of capturing small, frequent gains. Crypto markets often see quick reversals, so a smaller target increases the likelihood of hitting profits.

Use Candlestick Patterns (useCandlePatterns): True

Reasoning: Enabling candlestick patterns (e.g., engulfing, hammer) adds confirmation to signals, reducing false entries in choppy markets.

Use Volume Filter (useVolumeFilter): True

Reasoning: The volume filter ensures signals occur during high-volume breakouts, which are more likely to sustain in crypto markets.

Signal Arrow Size (signalSize): 2.0

Reasoning: Increasing the arrow size to 2.0 (from 1.5) makes buy/sell signals more visible on the chart, especially on smaller screens or volatile price action.

Background Highlight Transparency (bgTransparency): 85

Reasoning: A slightly higher transparency (85 from 80) keeps the background highlights subtle but visible, avoiding chart clutter.

How to Apply These Parameters

Copy the Script: Use the Pine Script provided in the previous response.

Paste in TradingView: Open TradingView, go to the Pine Editor, paste the code, and click "Add to Chart."

Set Parameters: In the strategy settings, manually input the recommended values above or adjust them via the input fields.

Test on a 5-Minute Chart: Apply the strategy to a liquid crypto pair (e.g., BTC/USDT, ETH/USDT) on a 5-minute chart.

Fine-Tuning for Optimal Performance

To find the absolute best parameters for your specific trading pair and market conditions, use TradingView’s Strategy Tester and optimization features:

Backtesting:

Run the strategy on historical data for your chosen pair (e.g., BTC/USDT on Binance).

Check metrics like Net Profit, Profit Factor, Win Rate, and Max Drawdown in the Strategy Tester.

Focus on a sample period of at least 1–3 months to capture various market conditions (bull, bear, sideways).

Parameter Optimization:

In the Strategy Tester, click the settings gear next to the strategy name.

Enable optimization for key inputs like emaFastLen (test range: 7–12), emaSlowLen (15–25), slPerc (0.5–1.5), and tpPerc (1.0–3.0).

Run the optimization to find the combination with the highest net profit or best Sharpe ratio, but avoid over-optimization (curve-fitting) by testing on out-of-sample data.

Market-Specific Adjustments:

Volatile Pairs (e.g., DOGE/USDT): Use tighter stop losses (e.g., 0.5–0.7%) and smaller take-profit targets (e.g., 1.0–1.2%) to account for rapid price swings.

Stable Pairs (e.g., BTC/USDT): Slightly wider stop losses (e.g., 1.0–1.2%) and take-profit targets (e.g., 1.8–2.5%) may work better.

Trending Markets: Increase emaSlowLen (e.g., to 25–30) to follow stronger trends.

Choppy Markets: Tighten bbMult (e.g., to 1.8) and lower rsiOverbought/rsiOversold (e.g., to 70/30) to filter noise.

Forward Testing:

After backtesting, run the strategy in real-time on a demo account for 1–2 weeks to validate performance under current market conditions.

Important Notes

No Universal "Best" Numbers: Optimal parameters vary by crypto pair, exchange, and market conditions (e.g., bull vs. bear market). The suggested values are a starting point based on common scalping practices.

Risk Management: Never risk more than 1–2% of your account per trade. Adjust position sizing in TradingView’s strategy settings to align with your risk tolerance.

Market Volatility: Crypto markets are highly volatile. Test the strategy on your specific pair and adjust parameters if signals are too frequent or too rare.

Not Financial Advice: This is an educational tool. Backtest thoroughly and use a demo account before trading with real funds.

If you want me to generate a chart showing backtest performance for specific parameters or to tweak the script further (e.g., adding more indicators or adjusting signal logic), let me know!can you add clear buy ans sell signs above the candles in this codeTo add clear buy and sell signals above the candles in the provided Pine Script, I'll modify the existing code to include prominent text labels directly above (for sell signals) and below (for buy signals) the candles. These labels will be larger, color-coded, and positioned to avoid clutter, ensuring they are easily visible on the chart. The core strategy logic (EMA, RSI, MACD, Bollinger Bands, candlestick patterns, and volume filter) will remain unchanged, and I'll reuse the same artifact_id since this is an update to the previous script.AdvancedCryptoScalpingStrategy.pinex-pine

Opening-Range BreakoutNote: Default trading date range looks mediocre. Set date range to "Entire History" to see full effect of the strategy. 50.91% profitable trades, 1.178 profit factor, steady profits and limited drawdown. Total P&L: $154,141.18, Max Drawdown: $18,624.36. High R^2

█ Overview

The Opening-Range Breakout strategy is a mechanical, session‑based day‑trading system designed to capture the initial burst of directional momentum immediately following the market open. It defines a user‑configurable “opening range” window, measures its high and low boundaries, then places breakout stop orders at those levels once the range closes. Built‑in filters on minimum range width, reward‑to‑risk ratios, and optional reversal logic help refine entries and manage risk dynamically.

█ How It Works

Opening‑Range Formation

Between 9:30–10:15 AM ET (configurable), the script tracks the highest high and lowest low to form the day’s opening range box.

On the first bar after the range window closes, the range high (OR_high) and low (OR_low) are “locked in.”

Range‑Width Filter

To avoid false breakouts in low‑volatility mornings, the range must be at least X% of the current price (default 0.35%).

If the measured opening-range width < minimum threshold, no orders are placed that day.

Entry & Order Placement

Long: a stop‑buy order at the opening‑range high.

Short: a stop‑sell order at the opening‑range low.

Only one side can trigger (or both if reverse logic is enabled after a losing trade).

Risk Management

Once triggered, each trade uses an ATR‑style stop-loss defined as a percentage retracement of the range (default 50% of range width).

Profit target is set at a configurable Reward/Risk Ratio (default 1.1×).

Optional: Reverse on Stop‑Loss – if the initial breakout loses, immediately reverse into the opposite side on the same day.

Session Exit

Any open positions are closed at the end of the regular trading day (default 3:45 PM ET window end, with hard flat at session close).

Visual cues are provided via green (range high) and red (range low) step‑line plots directly on the chart, allowing you to see the range box and breakout triggers in real time.

█ Why It Works

Early Momentum Capture: The first 15 – 60 minutes of trading encapsulate overnight news digestion and institutional order flow, creating a well‑defined volatility “range.”

Mechanical Discipline: Clear, rule‑based entries and exits remove emotional guesswork, ensuring consistency.

Volatility Filtering: By requiring a minimum range width, the system avoids choppy, low‑range days where false breakouts are common.

Dynamic Sizing: Stops and targets scale with the opening range, adapting automatically to each day’s volatility environment.

█ How to Use

Set Your Instruments & Timeframe

-Apply to any futures contract on a 1‑ to 5‑minute chart.

-Ensure chart timezone is set to America/New_York.

Configure Inputs

-Opening‑Range Window: e.g. “0930-1015” for a 45‑minute range.

-Min. OR Width (%): e.g. 0.35 for 0.35% of current price.

-Reward/Risk Ratio: e.g. 1.1 for a modest profit target above your stop.

-Max OR Retracement %: e.g. 50 to set stop at 50% of range width.

-One Trade Per Day: toggle to limit to a single breakout.

-Reverse on Stop Loss: toggle to flip direction after a losing breakout.

Monitor the Chart

-Watch the green and red range boundaries form during the session open.

-Orders will automatically submit on the first bar after the range window closes, conditioned on your filters.

Review & Adjust

-Backtest across multiple months to validate performance on your preferred contract.

-Tweak range duration, minimum width, and R/R multiple to fit your risk tolerance and desired win‑rate vs. expectancy balance.

█ Settings Reference

Input Defaults

Opening‑Range Window - Time window to form OR (HHMM-HHMM) - 0930–1015

Regular Trading Day - Full session for EOD flat (HHMM-HHMM) - 0930–1545

Min. OR Width (%) - Minimum OR size as % of close to trigger orders - 0.35

Reward/Risk Ratio - Profit target multiple of stop‑loss distance - 1.1

Max OR Retracement (%) - % of OR width to use as stop‑loss distance - 50

One Trade Per Day - Limit to a single breakout order per day - false

Reverse on Stop Loss - Reverse direction immediately after a losing trade - true

Disclaimer

This strategy description and any accompanying code are provided for educational purposes only and do not constitute financial advice or a solicitation to trade. Futures trading involves substantial risk, including possible loss of capital. Past performance is not indicative of future results. Traders should assess their own risk tolerance and conduct thorough backtesting and forward-testing before committing real capital.

BackTestLibLibrary "BackTestLib"

Allows backtesting indicator performance. Tracks typical metrics such as won/loss, profit factor, draw down, etc. Trading View strategy library provides similar (and more comprehensive)

functionality but only works with strategies. This libary was created to address performance tracking within indicators.

Two primary outputs are generated:

1. Summary Table: Displays overall performance metrics for the indicator over the chart's loaded timeframe and history

2. Details Table: Displays a table of individual trade entries and exits. This table can grow larger than the available chart space. It does have a max number of rows supported. I haven't

found a way to add scroll bars or scroll bar equivalents yet.

f_init(data, _defaultStopLoss, _defaultTakeProfit, _useTrailingStop, _useTraingStopToBreakEven, _trailingStopActivation, _trailingStopOffset)

f_init Initialize the backtest data type. Called prior to using the backtester functions

Parameters:

data (backtesterData) : backtesterData to initialize

_defaultStopLoss (float) : Default trade stop loss to apply

_defaultTakeProfit (float) : Default trade take profit to apply

_useTrailingStop (bool) : Trailing stop enabled

_useTraingStopToBreakEven (bool) : When trailing stop active, trailing stop will increase no further than the entry price

_trailingStopActivation (int) : When trailing stop active, trailing will begin once price exceeds base stop loss by this number of points

_trailingStopOffset (int) : When trailing stop active, it will trail the max price achieved by this number of points

Returns: Initialized data set

f_buildResultStr(_resultType, _price, _resultPoints, _numWins, _pointsWon, _numLoss, _pointsLost)

f_buildResultStr Helper function to construct a string of resutling data for exit tooltip labels

Parameters:

_resultType (string)

_price (float)

_resultPoints (float)

_numWins (int)

_pointsWon (float)

_numLoss (int)

_pointsLost (float)

f_buildResultLabel(data, labelVertical, labelOffset, long)

f_buildResultLabel Helper function to construct an Exit label for display on the chart

Parameters:

data (backtesterData)

labelVertical (bool)

labelOffset (int)

long (bool)

f_updateTrailingStop(_entryPrice, _curPrice, _sl, _tp, trailingStopActivationInput, trailingStopOffsetInput, useTrailingStopToBreakEven)

f_updateTrailingStop Helper function to advance the trailing stop as price action dictates

Parameters:

_entryPrice (float)

_curPrice (float)

_sl (float)

_tp (float)

trailingStopActivationInput (float)

trailingStopOffsetInput (float)

useTrailingStopToBreakEven (bool)

Returns: Updated stop loss for current price action

f_enterShort(data, entryPrice, fixedStopLoss)

f_enterShort Helper function to enter a short and collect data necessary for tracking the trade entry

Parameters:

data (backtesterData)

entryPrice (float)

fixedStopLoss (float)

Returns: Updated backtest data

f_enterLong(data, entryPrice, fixedStopLoss)

f_enterLong Helper function to enter a long and collect data necessary for tracking the trade entry

Parameters:

data (backtesterData)

entryPrice (float)

fixedStopLoss (float)

Returns: Updated backtest data

f_exitTrade(data)

f_enterLong Helper function to exit a trade and update/reset tracking data

Parameters:

data (backtesterData)

Returns: Updated backtest data

f_checkTradeConditionForExit(data, condition, curPrice, enableRealTime)

f_checkTradeConditionForExit Helper function to determine if provided condition indicates an exit

Parameters:

data (backtesterData)

condition (bool) : When true trade will exit

curPrice (float)

enableRealTime (bool) : When true trade will evaluate if barstate is relatime or barstate is confirmed; otherwise just checks on is confirmed

Returns: Updated backtest data

f_checkTrade(data, curPrice, curLow, curHigh, enableRealTime)

f_checkTrade Helper function to determine if current price action dictates stop loss or take profit exit

Parameters:

data (backtesterData)

curPrice (float)

curLow (float)

curHigh (float)

enableRealTime (bool) : When true trade will evaluate if barstate is relatime or barstate is confirmed; otherwise just checks on is confirmed

Returns: Updated backtest data

f_fillCell(_table, _column, _row, _title, _value, _bgcolor, _txtcolor, _text_size)

f_fillCell Helper function to construct result table cells

Parameters:

_table (table)

_column (int)

_row (int)

_title (string)

_value (string)

_bgcolor (color)

_txtcolor (color)

_text_size (string)

Returns: Table cell

f_prepareStatsTable(data, drawTesterSummary, drawTesterDetails, summaryTableTextSize, detailsTableTextSize, displayRowZero, summaryTableLocation, detailsTableLocation)

f_fillCell Helper function to populate result table

Parameters:

data (backtesterData)

drawTesterSummary (bool)

drawTesterDetails (bool)

summaryTableTextSize (string)

detailsTableTextSize (string)

displayRowZero (bool)

summaryTableLocation (string)

detailsTableLocation (string)

Returns: Updated backtest data

backtesterData

backtesterData - container for backtest performance metrics

Fields:

tradesArray (array) : Array of strings with entries for each individual trade and its results

pointsBalance (series float) : Running sum of backtest points won/loss results

drawDown (series float) : Running sum of backtest total draw down points

maxDrawDown (series float) : Running sum of backtest total draw down points

maxRunup (series float) : Running sum of max points won over the backtest

numWins (series int) : Number of wins of current backtes set

numLoss (series int) : Number of losses of current backtes set

pointsWon (series float) : Running sum of points won to date

pointsLost (series float) : Running sum of points lost to date

entrySide (series string) : Current entry long/short

tradeActive (series bool) : Indicates if a trade is currently active

tradeComplete (series bool) : Indicates if a trade just exited (due to stop loss or take profit)

entryPrice (series float) : Current trade entry price

entryTime (series int) : Current trade entry time

sl (series float) : Current trade stop loss

tp (series float) : Current trade take profit

defaultStopLoss (series float) : Default trade stop loss to apply

defaultTakeProfit (series float) : Default trade take profit to apply

useTrailingStop (series bool) : Trailing stop enabled

useTrailingStopToBreakEven (series bool) : When trailing stop active, trailing stop will increase no further than the entry price

trailingStopActivation (series int) : When trailing stop active, trailing will begin once price exceeds base stop loss by this number of points

trailingStopOffset (series int) : When trailing stop active, it will trail the max price achieved by this number of points

resultType (series string) : Current trade won/lost

exitPrice (series float) : Current trade exit price

resultPoints (series float) : Current trade points won/lost

summaryTable (series table) : Table to deisplay summary info

tradesTable (series table) : Table to display per trade info

Kaufman Trend Strategy# ✅ Kaufman Trend Strategy – Full Description (Script Publishing Version)

**Kaufman Trend Strategy** is a dynamic trend-following strategy based on Kaufman Filter theory.

It detects real-time trend momentum, reduces noise, and aims to enhance entry accuracy while optimizing risk.

⚠️ _For educational and research purposes only. Past performance does not guarantee future results._

---

## 🎯 Strategy Objective

- Smooth price noise using Kaufman Filter smoothing

- Detect the strength and direction of trends with a normalized oscillator

- Manage profits using multi-stage take-profits and adaptive ATR stop-loss logic

---

## ✨ Key Features

- **Kaufman Filter Trend Detection**

Extracts directional signal using a state space model.

- **Multi-Stage Profit-Taking**

Automatically takes partial profits based on color changes and zero-cross events.

- **ATR-Based Volatility Stops**

Stops adjust based on swing highs/lows and current market volatility.

---

## 📊 Entry & Exit Logic

**Long Entry**

- `trend_strength ≥ 60`

- Green trend signal

- Price above the Kaufman average

**Short Entry**

- `trend_strength ≤ -60`

- Red trend signal

- Price below the Kaufman average

**Exit (Long/Short)**

- Blue trend color → TP1 (50%)

- Oscillator crosses 0 → TP2 (25%)

- Trend weakens → Final exit (25%)

- ATR + swing-based stop loss

---

## 💰 Risk Management

- Initial capital: `$3,000`

- Order size: `$100` per trade (realistic, low-risk sizing)

- Commission: `0.002%`

- Slippage: `2 ticks`

- Pyramiding: `1` max position

- Estimated risk/trade: `~0.1–0.5%` of equity

> ⚠️ _No trade risks more than 5% of equity. This strategy follows TradingView script publishing rules._

---

## ⚙️ Default Parameters

- **1st Take Profit**: 50%

- **2nd Take Profit**: 25%

- **Final Exit**: 25%

- **ATR Period**: 14

- **Swing Lookback**: 10

- **Entry Threshold**: ±60

- **Exit Threshold**: ±40

---

## 📅 Backtest Summary

- **Symbol**: USD/JPY

- **Timeframe**: 1H

- **Date Range**: Jan 3, 2022 – Jun 4, 2025

- **Trades**: 924

- **Win Rate**: 41.67%

- **Profit Factor**: 1.108

- **Net Profit**: +$1,659.29 (+54.56%)

- **Max Drawdown**: -$1,419.73 (-31.87%)

---

## ✅ Summary

This strategy uses Kaufman filtering to detect market direction with reduced lag and increased smoothness.

It’s built with visual clarity and strong trade management, making it practical for both beginners and advanced users.

---

## 📌 Disclaimer

This script is for educational and informational purposes only and should not be considered financial advice.

Use with proper risk controls and always test in a demo environment before live trading.

Adaptive Fibonacci Pullback System -FibonacciFluxAdaptive Fibonacci Pullback System (AFPS) - FibonacciFlux

This work is licensed under a Attribution-NonCommercial-ShareAlike 4.0 International (CC BY-NC-SA 4.0). Original concepts by FibonacciFlux.

Abstract

The Adaptive Fibonacci Pullback System (AFPS) presents a sophisticated, institutional-grade algorithmic strategy engineered for high-probability trend pullback entries. Developed by FibonacciFlux, AFPS uniquely integrates a proprietary Multi-Fibonacci Supertrend engine (0.618, 1.618, 2.618 ratios) for harmonic volatility assessment, an Adaptive Moving Average (AMA) Channel providing dynamic market context, and a synergistic Multi-Timeframe (MTF) filter suite (RSI, MACD, Volume). This strategy transcends simple indicator combinations through its strict, multi-stage confluence validation logic. Historical simulations suggest that specific MTF filter configurations can yield exceptional performance metrics, potentially achieving Profit Factors exceeding 2.6 , indicative of institutional-level potential, while maintaining controlled risk under realistic trading parameters (managed equity risk, commission, slippage).

4 hourly MTF filtering

1. Introduction: Elevating Pullback Trading with Adaptive Confluence

Traditional pullback strategies often struggle with noise, false signals, and adapting to changing market dynamics. AFPS addresses these challenges by introducing a novel framework grounded in Fibonacci principles and adaptive logic. Instead of relying on static levels or single confirmations, AFPS seeks high-probability pullback entries within established trends by validating signals through a rigorous confluence of:

Harmonic Volatility Context: Understanding the trend's stability and potential turning points using the unique Multi-Fibonacci Supertrend.

Adaptive Market Structure: Assessing the prevailing trend regime via the AMA Channel.

Multi-Dimensional Confirmation: Filtering signals with lower-timeframe Momentum (RSI), Trend Alignment (MACD), and Market Conviction (Volume) using the MTF suite.

The objective is to achieve superior signal quality and adaptability, moving beyond conventional pullback methodologies.

2. Core Methodology: Synergistic Integration

AFPS's effectiveness stems from the engineered synergy between its core components:

2.1. Multi-Fibonacci Supertrend Engine: Utilizes specific Fibonacci ratios (0.618, 1.618, 2.618) applied to ATR, creating a multi-layered volatility envelope potentially resonant with market harmonics. The averaged and EMA-smoothed result (`smoothed_supertrend`) provides a robust, dynamic trend baseline and context filter.

// Key Components: Multi-Fibonacci Supertrend & Smoothing

average_supertrend = (supertrend1 + supertrend2 + supertrend3) / 3

smoothed_supertrend = ta.ema(average_supertrend, st_smooth_length)

2.2. Adaptive Moving Average (AMA) Channel: Provides dynamic market context. The `ama_midline` serves as a key filter in the entry logic, confirming the broader trend bias relative to adaptive price action. Extended Fibonacci levels derived from the channel width offer potential dynamic S/R zones.

// Key Component: AMA Midline

ama_midline = (ama_high_band + ama_low_band) / 2

2.3. Multi-Timeframe (MTF) Filter Suite: An optional but powerful validation layer (RSI, MACD, Volume) assessed on a lower timeframe. Acts as a **validation cascade** – signals must pass all enabled filters simultaneously.

2.4. High-Confluence Entry Logic: The core innovation. A pullback entry requires a specific sequence and validation:

Price interaction with `average_supertrend` and recovery above/below `smoothed_supertrend`.

Price confirmation relative to the `ama_midline`.

Simultaneous validation by all enabled MTF filters.

// Simplified Long Entry Logic Example (incorporates key elements)

long_entry_condition = enable_long_positions and

(low < average_supertrend and close > smoothed_supertrend) and // Pullback & Recovery

(close > ama_midline and close > ama_midline) and // AMA Confirmation

(rsi_filter_long_ok and macd_filter_long_ok and volume_filter_ok) // MTF Validation

This strict, multi-stage confluence significantly elevates signal quality compared to simpler pullback approaches.

1hourly filtering

3. Realistic Implementation and Performance Potential

AFPS is designed for practical application, incorporating realistic defaults and highlighting performance potential with crucial context:

3.1. Realistic Default Strategy Settings:

The script includes responsible default parameters:

strategy('Adaptive Fibonacci Pullback System - FibonacciFlux', shorttitle = "AFPS", ...,

initial_capital = 10000, // Accessible capital

default_qty_type = strategy.percent_of_equity, // Equity-based risk

default_qty_value = 4, // Default 4% equity risk per initial trade

commission_type = strategy.commission.percent,

commission_value = 0.03, // Realistic commission

slippage = 2, // Realistic slippage

pyramiding = 2 // Limited pyramiding allowed

)

Note: The default 4% risk (`default_qty_value = 4`) requires careful user assessment and adjustment based on individual risk tolerance.

3.2. Historical Performance Insights & Institutional Potential:

Backtesting provides insights into historical behavior under specific conditions (always specify Asset/Timeframe/Dates when sharing results):

Default Performance Example: With defaults, historical tests might show characteristics like Overall PF ~1.38, Max DD ~1.16%, with potential Long/Short performance variance (e.g., Long PF 1.6+, Short PF < 1).

Optimized MTF Filter Performance: Crucially, historical simulations demonstrate that meticulous configuration of the MTF filters (particularly RSI and potentially others depending on market) can significantly enhance performance. Under specific, optimized MTF filter settings combined with appropriate risk management (e.g., 7.5% risk), historical tests have indicated the potential to achieve **Profit Factors exceeding 2.6**, alongside controlled drawdowns (e.g., ~1.32%). This level of performance, if consistently achievable (which requires ongoing adaptation), aligns with metrics often sought in institutional trading environments.

Disclaimer Reminder: These results are strictly historical simulations. Past performance does not guarantee future results. Achieving high performance requires careful parameter tuning, adaptation to changing markets, and robust risk management.

3.3. Emphasizing Risk Management:

Effective use of AFPS mandates active risk management. Utilize the built-in Stop Loss, Take Profit, and Trailing Stop features. The `pyramiding = 2` setting requires particularly diligent oversight. Do not rely solely on default settings.

4. Conclusion: Advancing Trend Pullback Strategies

The Adaptive Fibonacci Pullback System (AFPS) offers a sophisticated, theoretically grounded, and highly adaptable framework for identifying and executing high-probability trend pullback trades. Its unique blend of Fibonacci resonance, adaptive context, and multi-dimensional MTF filtering represents a significant advancement over conventional methods. While requiring thoughtful implementation and risk management, AFPS provides discerning traders with a powerful tool potentially capable of achieving institutional-level performance characteristics under optimized conditions.

Acknowledgments

Developed by FibonacciFlux. Inspired by principles of Fibonacci analysis, adaptive averaging, and multi-timeframe confirmation techniques explored within the trading community.

Disclaimer

Trading involves substantial risk. AFPS is an analytical tool, not a guarantee of profit. Past performance is not indicative of future results. Market conditions change. Users are solely responsible for their decisions and risk management. Thorough testing is essential. Deploy at your own considered risk.

*Auto Backtest & Optimize EngineFull-featured Engine for Automatic Backtesting and parameter optimization. Allows you to test millions of different combinations of stop-loss and take profit parameters, including on any connected indicators.

⭕️ Key Futures

Quickly identify the optimal parameters for your strategy.

Automatically generate and test thousands of parameter combinations.

A simple Genetic Algorithm for result selection.

Saves time on manual testing of multiple parameters.

Detailed analysis, sorting, filtering and statistics of results.

Detailed control panel with many tooltips.

Display of key metrics: Profit, Win Rate, etc..

Comprehensive Strategy Score calculation.

In-depth analysis of the performance of different types of stop-losses.

Possibility to use to calculate the best Stop-Take parameters for your position.

Ability to test your own functions and signals.

Customizable visualization of results.

Flexible Stop-Loss Settings:

• Auto ━ Allows you to test all types of Stop Losses at once(listed below).

• S.VOLATY ━ Static stop based on volatility (Fixed, ATR, STDEV).

• Trailing ━ Classic trailing stop following the price.

• Fast Trail ━ Accelerated trailing stop that reacts faster to price movements.

• Volatility ━ Dynamic stop based on volatility indicators.

• Chandelier ━ Stop based on price extremes.

• Activator ━ Dynamic stop based on SAR.

• MA ━ Stop based on moving averages (9 different types).

• SAR ━ Parabolic SAR (Stop and Reverse).

Advanced Take-Profit Options:

• R:R: Risk/Reward ━ sets TP based on SL size.

• T.VOLATY ━ Calculation based on volatility indicators (Fixed, ATR, STDEV).

Testing Modes:

• Stops ━ Cyclical stop-loss testing

• Pivot Point Example ━ Example of using pivot points

• External Example ━ Built-in example how test functions with different parameters

• External Signal ━ Using external signals

⭕️ Usage

━ First Steps:

When opening, select any point on the chart. It will not affect anything until you turn on Manual Start mode (more on this below).

The chart will immediately show the best results of the default Auto mode. You can switch Part's to try to find even better results in the table.

Now you can display any result from the table on the chart by entering its ID in the settings.

Repeat steps 3-4 until you determine which type of Stop Loss you like best. Then set it in the settings instead of Auto mode.

* Example: I flipped through 14 parts before I liked the first result and entered its ID so I could visually evaluate it on the chart.

Then select the stop loss type, choose it in place of Auto mode and repeat steps 3-4 or immediately follow the recommendations of the algorithm.

Now the Genetic Algorithm at the bottom right will prompt you to enter the Parameters you need to search for and select even better results.

Parameters must be entered All at once before they are updated. Enter recommendations strictly in fields with the same names.

Repeat steps 5-6 until there are approximately 10 Part's left or as you like. And after that, easily pour through the remaining Parts and select the best parameters.

━ Example of the finished result.

━ Example of use with Takes

You can also test at the same time along with Take Profit. In this example, I simply enabled Risk/Reward mode and immediately specified in the TP field Maximum RR, Minimum RR and Step. So in this example I can test (3-1) / 0.1 = 20 Takes of different sizes. There are additional tips in the settings.

━

* Soon you will start to understand how the system works and things will become much easier.

* If something doesn't work, just reset the engine settings and start over again.

* Use the tips I have left in the settings and on the Panel.

━ Details:

Sort ━ Sorting results by Score, Profit, Trades, etc..

Filter ━ Filtring results by Score, Profit, Trades, etc..

Trade Type ━ Ability to disable Long\Short but only from statistics.

BackWin ━ Backtest Window Number of Candle the script can test.

Manual Start ━ Enabling it will allow you to call a Stop from a selected point. which you selected when you started the engine.

* If you have a real open position then this mode can help to save good Stop\Take for it.

1 - 9 Сheckboxs ━ Allow you to disable any stop from Auto mode.

Ex Source - Allow you to test Stops/Takes from connected indicators.

Connection guide:

//@version=6

indicator("My script")

rsi = ta.rsi(close, 14)

buy = not na(rsi) and ta.crossover (rsi, 40) // OS = 40

sell = not na(rsi) and ta.crossunder(rsi, 60) // OB = 60

Signal = buy ? +1 : sell ? -1 : 0

plot(Signal, "🔌Connector🔌", display = display.none)

* Format the signal for your indicator in a similar style and then select it in Ex Source.

⭕️ How it Works

Hypothesis of Uniform Distribution of Rare Elements After Mixing.

'This hypothesis states that if an array of N elements contains K valid elements, then after mixing, these valid elements will be approximately uniformly distributed.'

'This means that in a random sample of k elements, the proportion of valid elements should closely match their proportion in the original array, with some random variation.'

'According to the central limit theorem, repeated sampling will result in an average count of valid elements following a normal distribution.'

'This supports the assumption that the valid elements are evenly spread across the array.'

'To test this hypothesis, we can conduct an experiment:'

'Create an array of 1,000,000 elements.'

'Select 1,000 random elements (1%) for validation.'

'Shuffle the array and divide it into groups of 1,000 elements.'

'If the hypothesis holds, each group should contain, on average, 1~ valid element, with minor variations.'

* I'd like to attach more details to My hypothesis but it won't be very relevant here. Since this is a whole separate topic, I will leave the minimum part for understanding the engine.

Practical Application

To apply this hypothesis, I needed a way to generate and thoroughly mix numerous possible combinations. Within Pine, generating over 100,000 combinations presents significant challenges, and storing millions of combinations requires excessive resources.

I developed an efficient mechanism that generates combinations in random order to address these limitations. While conventional methods often produce duplicates or require generating a complete list first, my approach guarantees that the first 10% of possible combinations are both unique and well-distributed. Based on my hypothesis, this sampling is sufficient to determine optimal testing parameters.

Most generators and randomizers fail to accommodate both my hypothesis and Pine's constraints. My solution utilizes a simple Linear Congruential Generator (LCG) for pseudo-randomization, enhanced with prime numbers to increase entropy during generation. I pre-generate the entire parameter range and then apply systematic mixing. This approach, combined with a hybrid combinatorial array-filling technique with linear distribution, delivers excellent generation quality.

My engine can efficiently generate and verify 300 unique combinations per batch. Based on the above, to determine optimal values, only 10-20 Parts need to be manually scrolled through to find the appropriate value or range, eliminating the need for exhaustive testing of millions of parameter combinations.

For the Score statistic I applied all the same, generated a range of Weights, distributed them randomly for each type of statistic to avoid manual distribution.

Score ━ based on Trade, Profit, WinRate, Profit Factor, Drawdown, Sharpe & Sortino & Omega & Calmar Ratio.

⭕️ Notes

For attentive users, a little tricks :)

To save time, switch parts every 3 seconds without waiting for it to load. After 10-20 parts, stop and wait for loading. If the pause is correct, you can switch between the rest of the parts without loading, as they will be cached. This used to work without having to wait for a pause, but now it does slower. This will save a lot of time if you are going to do a deeper backtest.

Sometimes you'll get the error “The scripts take too long to execute.”

For a quick fix you just need to switch the TF or Ticker back and forth and most likely everything will load.

The error appears because of problems on the side of the site because the engine is very heavy. It can also appear if you set too long a period for testing in BackWin or use a heavy indicator for testing.

Manual Start - Allow you to Start you Result from any point. Which in turn can help you choose a good stop-stick for your real position.

* It took me half a year from idea to current realization. This seems to be one of the few ways to build something automatic in backtest format and in this particular Pine environment. There are already better projects in other languages, and they are created much easier and faster because there are no limitations except for personal PC. If you see solutions to improve this system I would be glad if you share the code. At the moment I am tired and will continue him not soon.

Also You can use my previosly big Backtest project with more manual settings(updated soon)

Gold Pro StrategyHere’s the strategy description in a chat format:

---

**Gold (XAU/USD) Trend-Following Strategy**

This **trend-following strategy** is designed for trading gold (XAU/USD) by combining moving averages, MACD momentum indicators, and RSI filters to capture sustained trends while managing volatility risks. The strategy uses volatility-adjusted stops to protect gains and prevent overexposure during erratic price movements. The aim is to take advantage of trending markets by confirming momentum and ensuring entries are not made at extreme levels.

---

**Key Components**

1. **Trend Identification**

- **50 vs 200 EMA Crossover**

- **Bullish Trend:** 50 EMA crosses above 200 EMA, and the price closes above the 200 EMA

- **Bearish Trend:** 50 EMA crosses below 200 EMA, and the price closes below the 200 EMA

2. **Momentum Confirmation**

- **MACD (12,26,9)**

- **Buy Signal:** MACD line crosses above the signal line

- **Sell Signal:** MACD line crosses below the signal line

- **RSI (14 Period)**

- **Bullish Zone:** RSI between 50-70 to avoid overbought conditions

- **Bearish Zone:** RSI between 30-50 to avoid oversold conditions

3. **Entry Criteria**

- **Long Entry:** Bullish trend, MACD bullish crossover, and RSI between 50-70

- **Short Entry:** Bearish trend, MACD bearish crossover, and RSI between 30-50

4. **Exit & Risk Management**

- **ATR Trailing Stops (14 Period):**

- Initial Stop: 3x ATR from entry price

- Trailing Stop: Adjusts to lock in profits as price moves favorably

- **Position Sizing:** 100% of equity per trade (high-risk strategy)

---

**Key Logic Flow**

1. **Trend Filter:** Use the 50/200 EMA relationship to define the market's direction

2. **Momentum Confirmation:** Confirm trend momentum with MACD crossovers

3. **RSI Validation:** Ensure RSI is within non-extreme ranges before entering trades

4. **Volatility-Based Risk Management:** Use ATR stops to manage market volatility

---

**Visual Cues**

- **Blue Line:** 50 EMA

- **Red Line:** 200 EMA

- **Green Triangles:** Long entry signals

- **Red Triangles:** Short entry signals

---

**Strengths**

- **Clear Trend Focus:** Avoids counter-trend trades

- **RSI Filter:** Prevents entering overbought or oversold conditions

- **ATR Stops:** Adapts to gold’s inherent volatility

- **Simple Rules:** Easy to follow with minimal inputs

---

**Weaknesses & Risks**

- **Infrequent Signals:** 50/200 EMA crossovers are rare

- **Potential Missed Opportunities:** Strict RSI criteria may miss some valid trends

- **Aggressive Position Sizing:** 100% equity allocation can lead to large drawdowns

- **No Profit Targets:** Relies on trailing stops rather than defined exit targets

---

**Performance Profile**

| Metric | Expected Range |

|----------------------|---------------------|

| Annual Trades | 4-8 |

| Win Rate | 55-65% |

| Max Drawdown | 25-35% |

| Profit Factor | 1.8-2.5 |

---

**Optimization Recommendations**

1. **Increase Trade Frequency**

Adjust the EMAs to shorter periods:

- `emaFastLen = input.int(30, "Fast EMA")`

- `emaSlowLen = input.int(150, "Slow EMA")`

2. **Relax RSI Filters**

Adjust the RSI range to:

- `rsiBullish = rsi > 45 and rsi < 75`

- `rsiBearish = rsi < 55 and rsi > 25`

3. **Add Profit Targets**

Introduce a profit target at 1.5% above entry:

```pine

strategy.exit("Long Exit", "Long",

stop=longStopPrice,

profit=close*1.015, // 1.5% target

trail_offset=trailOffset)

```

4. **Reduce Position Sizing**

Risk a smaller percentage per trade:

- `default_qty_value=25`

---

**Best Use Case**

This strategy excels in **strong trending markets** such as gold rallies during economic or geopolitical crises. However, during sideways or choppy market conditions, the strategy might require manual intervention to avoid false signals. Additionally, integrating fundamental analysis—like monitoring USD weakness or geopolitical risks—can enhance its effectiveness.

---

This strategy offers a balanced approach for trading gold, combining trend-following principles with risk management tailored to the volatility of the market.

Mean Reversion Pro Strategy [tradeviZion]Mean Reversion Pro Strategy : User Guide

A mean reversion trading strategy for daily timeframe trading.

Introduction

Mean Reversion Pro Strategy is a technical trading system that operates on the daily timeframe. The strategy uses a dual Simple Moving Average (SMA) system combined with price range analysis to identify potential trading opportunities. It can be used on major indices and other markets with sufficient liquidity.

The strategy includes:

Trading System

Fast SMA for entry/exit points (5, 10, 15, 20 periods)

Slow SMA for trend reference (100, 200 periods)

Price range analysis (20% threshold)

Position management rules

Visual Elements

Gradient color indicators

Three themes (Dark/Light/Custom)

ATR-based visuals

Signal zones

Status Table

Current position information

Basic performance metrics

Strategy parameters

Optional messages

📊 Strategy Settings

Main Settings

Trading Mode

Options: Long Only, Short Only, Both

Default: Long Only

Position Size: 10% of equity

Starting Capital: $20,000

Moving Averages

Fast SMA: 5, 10, 15, or 20 periods

Slow SMA: 100 or 200 periods

Default: Fast=5, Slow=100

🎯 Entry and Exit Rules

Long Entry Conditions

All conditions must be met:

Price below Fast SMA

Price below 20% of current bar's range

Price above Slow SMA

No existing position

Short Entry Conditions

All conditions must be met:

Price above Fast SMA

Price above 80% of current bar's range

Price below Slow SMA

No existing position

Exit Rules

Long Positions

Exit when price crosses above Fast SMA

No fixed take-profit levels

No stop-loss (mean reversion approach)

Short Positions

Exit when price crosses below Fast SMA

No fixed take-profit levels

No stop-loss (mean reversion approach)

💼 Risk Management

Position Sizing

Default: 10% of equity per trade

Initial capital: $20,000

Commission: 0.01%

Slippage: 2 points

Maximum one position at a time

Risk Control

Use daily timeframe only

Avoid trading during major news events

Consider market conditions

Monitor overall exposure

📊 Performance Dashboard

The strategy includes a comprehensive status table displaying:

Strategy Parameters

Current SMA settings

Trading direction

Fast/Slow SMA ratio

Current Status

Active position (Flat/Long/Short)

Current price with color coding

Position status indicators

Performance Metrics

Net Profit (USD and %)

Win Rate with color grading

Profit Factor with thresholds

Maximum Drawdown percentage

Average Trade value

📱 Alert Settings

Entry Alerts

Long Entry (Buy Signal)

Short Entry (Sell Signal)

Exit Alerts

Long Exit (Take Profit)

Short Exit (Take Profit)

Alert Message Format

Strategy name

Signal type and direction

Current price

Fast SMA value

Slow SMA value

💡 Usage Tips

Consider starting with Long Only mode

Begin with default settings

Keep track of your trades

Review results regularly

Adjust settings as needed

Follow your trading plan

⚠️ Disclaimer

This strategy is for educational and informational purposes only. It is not financial advice. Always:

Conduct your own research

Test thoroughly before live trading

Use proper risk management

Consider your trading goals

Monitor market conditions

Never risk more than you can afford to lose

📋 Release Notes

14 January 2025

Added New Fast & Slow SMA Options:

Fibonacci-based periods: 8, 13, 21, 144, 233, 377

Additional period: 50

Complete Fast SMA options now: 5, 8, 10, 13, 15, 20, 21, 34, 50

Complete Slow SMA options now: 100, 144, 200, 233, 377

Bug Fixes:

Fixed Maximum Drawdown calculation in the performance table

Now using strategy.max_drawdown_percent for accurate DD reporting

Previous version showed incorrect DD values

Performance metrics now accurately reflect trading results

Performance Note:

Strategy tested with Fast/Slow SMA 13/377

Test conducted with 10% equity risk allocation

Daily Timeframe

For Beginners - How to Modify SMA Levels:

Find this line in the code:

fastLength = input.int(title="Fast SMA Length", defval=5, options= )

To add a new Fast SMA period: Add the number to the options list, e.g.,

To remove a Fast SMA period: Remove the number from the options list

For Slow SMA, find:

slowLength = input.int(title="Slow SMA Length", defval=100, options= )

Modify the options list the same way

⚠️ Note: Keep the periods that make sense for your trading timeframe

💡 Tip: Test any new combinations thoroughly before live trading

"Trade with Discipline, Manage Risk, Stay Consistent" - tradeviZion

Backtest any Indicator v5Happy Trade,

here you get the opportunity to backtest any of your indicators like a strategy without converting them into a strategy. You can choose to go long or go short and detailed time filters. Further more you can set the take profit and stop loss, initial capital, quantity per trade and set the exchange fees. You get an overall result table and even a detailed, scroll-able table with all trades. In the Image 1 you see the provided info tables about all Trades and the Result Summary. Further more every trade is marked by a background color, Labels and Levels. An opening Label with the trade direction and trade number. A closing Label again with the trade number, the trades profit in % and the total amount of $ after all past trades. A green line for the take profit level and a red line for the stop loss.

Image 1

Example

For this description we choose the Stochastic RSI indicator from TradingView as it is. In Image 2 is shown the performance of it with decent settings.

Timeframe=45, BTCUSD, 2023-08-01 - 2023-10-20

Stoch RSI: k=30, d=40, RSI-length=140, stoch-length=140

Backtest any Indicator: input signal=Stoch RSI, goLong, take profit=9.1%, stop loss=2.5%, start capital=1000$, qty=5%, fee=0.1%, no Session Filter

Image 2

Usage

1) You need to know the name of the boolean (or integer) variable of your indicator which hold the buy condition. Lets say that this boolean variable is called BUY. If this BUY variable is not plotted on the chart you simply add the following code line at the end of your pine script.

For boolean (true/false) BUY variables use this:

plot(BUY ? 1:0,'Your buy condition hold in that variable BUY',display = display.data_window)

And in case your script's BUY variable is an integer or float then use instate the following code line:

plot(BUY ,'Your buy condition hold in that variable BUY',display = display.data_window)

2) Probably the name of this BUY variable in your indicator is not BUY. Simply replace in the code line above the BUY with the name of your script's trade condition variable.

3) Save your changed Indicator script.

4) Then add this 'Backtest any Indicator' script to the chart ...

5) and go to the settings of it. Choose under "Settings -> Buy Signal" your Indicator. So in the example above choose .

The form is usually: ' : BUY'. Then you see something like Image 2

6) Decide which trade direction the BUY signal should trigger. A go Long or a go Short by set the hook or not.

Now you have a backtest of your Indicator without converting it into a strategy. You may change the setting of your Indicator to the best results and setup the following strategy settings like Time- and Session Filter, Stop Loss, Take Profit etc. More of it below in the section Settings Menu.

Appereance

In the Image 2 you see on the right side the List of Trades . To scroll down you go into the settings again and decrease the scroll value. So you can see all trades that have happened before. In case there is an open trade you will find it at the last position of the list.

Every Long trade is green back grounded while Short trades are red.

Every trade begins with a label that show goLong or goShort and its number. And ends with another label again with its number, Profit in % and the resulting total amount of cash.

If activated you further see the Take Profit as a green line and the Stop Loss as a orange line. In the settings you can set their percentage above or below the entry price.

You also see the Result Summary below. Here you find the usual stats of a strategy of all closed trades. The profit after total amount of fees , amount of trades, Profit Factor and the total amount of fees .

Settings Menu

In the settings menu you will find the following high-lighted sections. Most of the settings have a question mark on their right side. Move over it with the cursor to read specific explanation.

Input Signal of your Indicator: Under Buy you set the trade signal of your Indicator. And under Target you set the value when a trade should happen. In the Example with the Stochastic RSI above we used 20. Below you can set the trade direction, let it be go short when hooked or go long when unhooked.

Trade Settings & List of Trades: Take Profit set the target price of any trade. Stop Loss set the price to step out when a trade goes the wrong direction. Check mark the List of Trades to see any single trade with their stats. In case that there are more trades as fits in the list you can scroll down the list by decrease the value Scroll .

Time Filter: You can set a Start Time or deactivate it by leave it unhooked. The same with End Time .

Session Filter: here you can choose to activate it on weekly base. Which days of the week should be trading and those without. And also on daily base from which time on and until trade are possible. Outside of all times and sessions there will be no new trades if activated.

Invest Settings: here you can choose the amount of cash to start with. The Quantity percentage define for every trade how much of the cash should be invested and the Fee percentage which have to be payed every trade. Open position and closing position.

Other Announcements

This Backtest script don't use the strategy functions of TradingView. It is programmed as an indicator. All trades get executed at candle closing. This script use the functionality "Indicator-on-Indicator" from TradingView.

Conclusion

So now it is your turn, take your promising indicators and connect it to that Backtest script. With it you get a fast impression of how successful your indicator will trade. You don't have to relay on coders who maybe add cheating code lines. Further more you can check with the Time Filter under which market condition you indicator perform the best or not so well. Also with the Session Filter you can sort out repeating good market conditions for your indicator. Even you can check with the GoShort XOR GoLong check mark the trade signals of you indicator in opposite trade direction with one click. And compare your indicators under the same conditions and get the results just after 2 clicks. Thanks to the in-build fee setting you get an impression how much a 0.1% fee cost you in total.

Cheers

Strategy Myth-Busting #20 - HalfTrend+HullButterfly - [MYN]#20 on the Myth-Busting bench, we are automating the " I Found Super Easy 1 Minute Scalping System And Backtest It 100 Times " strategy from " Jessy Trading " who claims 30.58% net profit over 100 trades in a couple of weeks with a 51% win rate and profit factor of 1.56 on EURUSD .

This one surprised us quite a bit. Despite the title of this strategy indicating this is on the 1 min timeframe, the author demonstrates the backtesting manually on the 5 minute timeframe. Given the simplicity of this strategy only incorporating a couple of indicators, it's robustness being able to be profitable in both low and high timeframes and on multiple symbols was quite refreshing.

The 3 settings which we need to pay most attention to here is the Hull Butterfly length, HalfTrend amplitude and the Max Number Of Bars Between Hull and HalfTrend Trigger. Depending on the timeframe and symbol, these settings greatly impact the performance outcomes of the strategy. I've listed a couple of these below.

And as always, If you know of or have a strategy you want to see myth-busted or just have an idea for one, please feel free to message me.

This strategy uses a combination of 3 open-source public indicators:

Hull Butterfly Oscillator by LuxAlgo

HalfTrend by Everget

Trading Rules

5 min candles but higher / lower candles work too.

Stop loss at swing high/low

Take Profit 1.5x the risk

Long

Hull Butterfly gives us green column, Wait for HalfTrend to present an up arrow and enter trade.

Short

Hull Butterfly gives us a red column , Wait for HalfTrend to present a down arrow and enter trade.

Alternative Trading Settings for different time frames

1 Minute Timeframe

Move the Hull Butterfly length from the default 11 to 9

Move the HalfTrend Amplitude from the default 2 to 1

Enabling ADX Filter with a 25 threshold

2 Hour Timeframe

Move the HalfTrend Amplitude from the default 2 to 1

Laddered Take Profits from 14.5% to 19% with an 8% SL

SUPPORT RESISTANCE STRATEGY [5MIN TF]A SUPPORT RESISTANCE BREAKOUT STRATEGY for 5 minute Time-Frame , that has the time condition for Indian Markets

The Timing can be changed to fit other markets, scroll down to "TIME CONDITION" to know more.

The commission is also included in the strategy .

The basic idea is when ,

1) Price crosses above Resistance Level ,indicated by Red Line, is a Long condition.

2) Price crosses below Support Level ,indicated by Green Line , is a Short condition.

3) Candle high crosses above ema1, is a part of the Long condition .

4) Candle low crosses below ema1, is a part of the Short condition .

5) Volume Threshold is an added confirmation for long/short positions.

6) Maximum Risk per trade for the intraday trade can be changed .

7) Default qty size is set to 50 contracts , which can be changed under settings → properties → order size.

8) ATR is used for trailing after entry, as mentioned in the inputs below.

// ═════════════════════════//

// ————————> INPUTS <————————— //

// ═════════════════════════//

→ L_Bars ———————————> Length of Resistance / Support Levels.

→ R_Bars ———————————> Length of Resistance / Support Levels.

→ Volume Break ———————> Volume Breakout from range to confirm Long/Short position.

→ Price Cross Ema —————> Added condition as explained above (3) and (4).

→ ATR LONG —————————> ATR stoploss trail for Long positions.

→ ATR SHORT ————————> ATR stoploss trail for Short positions.

→ RISK ————————————> Maximum Risk per trade intraday.

The strategy was back-tested on TCS ,the input values and the results are mentioned under "BACKTEST RESULTS" below.

// ═════════════════════════ //

// ————————> PROPERTIES<——————— //

// ═════════════════════════ //

Default_qty_size ————> 50 contracts , which can be changed under

Settings

↓

Properties

↓

Order size

// ═══════════════════════════════//

// ————————> TIME CONDITION <————————— //

// ═══════════════════════════════//

The time can be changed in the script , Add it → click on ' { } ' → Pine editor→ making it a copy [right top corner} → Edit the line 27.

The Indian Markets open at 9:15am and closes at 3:30pm.

The 'time_cond' specifies the time at which Entries should happen .

"Close All" function closes all the trades at 3pm , at the open of the next candle.

To change the time to close all trades , Go to Pine Editor → Edit the line 92 .

All open trades get closed at 3pm , because some brokers don't allow you to place fresh intraday orders after 3pm .

// ═══════════════════════════════════════════════ //

// ————————> BACKTEST RESULTS ( 100 CLOSED TRADES )<————————— //

// ═══════════════════════════════════════════════ //

INPUTS can be changed for better Back-Test results.

The strategy applied to NSE:TCS ( 5 min Time-Frame and contract size 50) gives us 60% profitability , as shown below

It was tested for a period a 6 months with a Profit Factor of 1.8 ,net Profit of 30,000 Rs profit .

Sharpe Ratio : 0.49

Sortino Ratio : 1.4

The graph has a Linear Curve with Consistent Profits.

The INPUTS are as follows,

1) L_Bars —————————> 4

2) R_Bars —————————> 4

3) Volume Break ————> 5

4) Price Cross Ema ——> 100

5) ATR LONG ——————> 2.4

6) ATR SHORT —————> 2.6

7) RISK —————————> 2000

8) Default qty size ——> 50

NSE:TCS

Save it to favorites.

Apply it to your charts Now !!

Thank You ☺ NSE:TCS

PIVOT STRATEGY [INDIAN MARKET TIMING]

A Back-tested Profitable Strategy for Free!!

A PIVOT INTRADAY STRATEGY for 5 minute Time-Frame , that also explains the time condition for Indian Markets

The Timing can be changed to fit other markets, scroll down to "TIME CONDITION" to know more.

The commission is also included in the strategy .

The basic idea is when ,

1) Price crosses above ema1 ,indicated by pivot highest line in green color .

2) Price crosses below ema1 ,indicated by pivot lowest line in red color .

3) Candle high crosses above pivot highest , is the Long condition .

4) Candle low crosses below pivot lowest , is the Short condition .

5) Maximum Risk per trade for the intraday trade can be changed .

6) Default_qty_size is set to 60 contracts , which can be changed under settings → properties → order size .

7) ATR is used for trailing after entry, as mentioned in the inputs below.

// ═════════════════════════//

// ————————> INPUTS <————————— //

// ═════════════════════════//

Leftbars —————> Length of pivot highs and lows

Rightbars —————> Length of pivot highs and lows

Price Cross Ema —————> Added condition

ATR LONG —————> ATR stoploss trail for Long positions

ATR SHORT —————> ATR stoploss trail for Short positions

RISK —————> Maximum Risk per trade for the day

The strategy was back-tested on RELIANCE ,the input values and the results are mentioned under "BACKTEST RESULTS" below .

// ═════════════════════════ //

// ————————> PROPERTIES<——————— //

// ═════════════════════════ //

Default_qty_size ————> 60 contracts , which can be changed under settings

↓

properties

↓

order size

// ═══════════════════════════════//

// ————————> TIME CONDITION <————————— //

// ═══════════════════════════════//

The time can be changed in the script , Add it → click on ' { } ' → Pine editor→ making it a copy [right top corner} → Edit the line 25 .

The Indian Markets open at 9:15am and closes at 3:30pm .

The 'time_cond' specifies the time at which Entries should happen .

"Close All" function closes all the trades at 3pm, at the open of the next candle.

To change the time to close all trades , Go to Pine Editor → Edit the line 103 .

All open trades get closed at 3pm , because some brokers don't allow you to place fresh intraday orders after 3pm .

NSE:RELIANCE

// ═══════════════════════════════════════════════ //

// ————————> BACKTEST RESULTS ( 128 CLOSED TRADES )<————————— //

// ═══════════════════════════════════════════════ //

INPUTS can be changed for better back-test results.

The strategy applied to NIFTY ( 5 min Time-Frame and contract size 60 ) gives us 60% profitability y , as shown below

It was tested for a period a 6 months with a Profit Factor of 1.45 ,net Profit of 21,500Rs profit .

Sharpe Ratio : 0.311

Sortino Ratio : 0.727

The graph has a Linear Curve with consistent profits .

The INPUTS are as follows,

1) Leftbars ————————> 3

2) Rightbars ————————> 5

3) Price Cross Ema ——————> 150

4) ATR LONG ————————> 2.7

5) ATR SHORT ———————> 2.9

6) RISK —————————> 2500

7) Default qty size ——————> 60

NSE:RELIANCE

Save it to favorites.

Apply it to your charts Now !!

↓

FOLLOW US FOR MORE !

Thank me later ;)

TUE ADX/MACD Confluence V1.0The ADX and MACD confluence can be a powerful predictor in stock movements. This script will help you find those confluences in an easy to understand visual manner.

It includes Buy and Sell signals for detected confluences, and will show colored candles to help you determine when to exit a trade. When the candles turn to white that means the detected confluence is no longer in play and you may want to consider a trailing stop loss.

The Buy and Sell signals will display on the first occurrence of each confluence.

It's important to understand that both of these are lagging indicators, but with a careful attention to your stoploss you can easily generate a positive profit factor.

This code is provided open source and you're free to use it for any purpose other than resale.

BB21_MA200_StrategyThis strategy follows the trend and keeps you in the trend until it breaks SMA 200

SMA setting is 200

BB setting is 21

BUY

====

when BB is (lower band and upper band) above SMA 200 and price crossing above BB middle line

Partial Exit

==========

When Lower BB crossing down SMA200 , exit 30%

Total Exit

=========

When BB middle band crosses down SMA200 , exit ALL

Stop Loss

======

default is set to 5%

Risk Management

================

This is new parameter I have introduced in my strategies. Default value is 10% . That means , if your capital is 10000 , you are willing to risk 10% of it ... i.e 1000.

It doesnot mean that you are buying shares/units for 1000 only. It is different ...see below

Your trade size is calculated based on Risk% .... capital x risk 5 / stop Loss units

for further explanation you can check Alexander Elder's risk management rule. He mentioned 2% rule for 100K account. But most of us dont have 100K accounts .. . so I have defaulted 10% on 10K account. You can change this values and see the results. It wont change the number of trades or profit factor. It will increase the net profit.

Warning

=======

For educational purposes only

FTSMA - Trend is your frendThis my new solid strategy: if you belive that "TREND IS YOUR FRIEND" this is for you!

I have tested with many pairs and at many timeframes and have profit with just minor changes in settings.

I suggest to use it for intraday trading .

VERY IMPORTANT NOTE: this is a trend following strategy, so the target is to stay in the trade as much as possible. If your trading style is more focused on scalping and/or pullbaks, this strategy is not for you.

This strategy uses moving averages applied to Fourier waves for forecasting trend direction.

How strategy works:

- Buy when fast MA is above mid MA and price is above slow MA, which acts as a trend indicator.

- Sell when fast MA is below mid MA and price is below slow MA, which acts as a trend indicator.

Strategy uses a lot of pyramiding orders because when you are in a flat market phase it will close 1 or 2 orders with a loss, but when a big trend starts, it will have profit in a lot of orders.

So, if you analize carefully the strategy results, you will note that "Percent Profitable" is very low (30% in this case) because strategy opened a lot of orders also in flat markets with small losses, BUT "Avg # bars in winning trades" is very high and overall Profit is very high: when a big trend starts, orders are kept open for long time generating big profits.

Thanks to all pinescripters mentioned in the code for their snippets.

I have also a study with alerts. Next improvement (only to whom is interested to this script and follows me): study with alerts on multiple tickers all at one. Leave a comment if you want to have access to study.

HOW TO USE STRATEGY AND STUDY TOGHETER:

1- Add to chart the strategy first, so your workspace will be as clean as possible.

2- Open the Strategy Tester tab at footer of the page.

3- Modify settings to get best results (Profit, Profit Factor, Drawdown).

4- Add study with alerts to your chart with same setting of strategy.

I WILL PROVIDE A DETAILED QUICK INSTALLATION GUIDE WITH THE STUDY!

Please use comment section for any feedback or contact me if you need support.

Patient Trendfollower (7)(alpha)Patient Trendfollower consists of 21 and 55 EMA, Commodity Channel Index and Supertrend indicator. It confirms a trend and gives you a signal on a pullback. Original creation worked on 1h EURUSD chart.

►Long setup:

• 21 EMA is above 55 EMA, which is above the Supertrend indicator.